A wise strategy for claiming Social Security benefits may result in additional retirement income.

About Social Security

Social Security retirement benefits help provide lifetime, inflation-adjusted income. Combined with your retirement savings, plus any pension benefits you may receive, Social Security may serve as an important component of your overall plan for retirement income.

When Can You Claim Social Security?

Eligibility for Social Security begins "early", at age 62. However, claiming early will reduce your monthly check - permanently. There are many issues to consider when deciding to claim benefits.

Two Key Terms: PIA and FRA

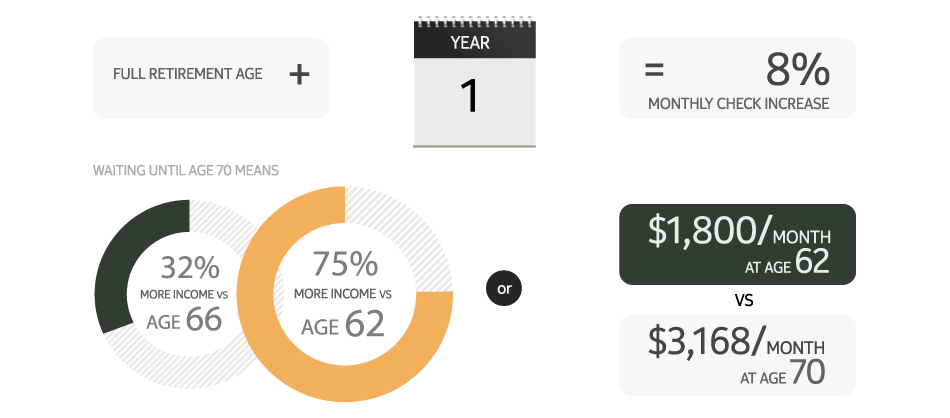

Your Primary Insurance Amount, or PIA, is the amount of monthly income you will receive at your normal retirement age, also known as your Full Retirement Age (FRA). Depending upon when you were born, your FRA will range from age 65 to age 67. People born between 1943 and 1954 have an FRA of 66. Click here to see your FRA.

Your PIA, which is based upon your lifetime earnings, may be reduced or increased, depending upon when you decide to claim retirement benefits. You may claim benefits before reaching your FRA, as early as age 62, and you may delay claiming until after your FRA, as late as age 70.

Claiming after you've reached your FRA offers benefits. Your monthly check will be increased by 8% for each year that you delay, up to age 70. For example, if your FRA is 66, and you delay four years until you're 70, your monthly check will be 32% higher than at age 66, and 75% higher than at age 62. Over time, one might receive significantly more dollars depending upon when benefits are claimed.

You may benefit from seeking the advice of a financial advisor that focuses on retirement income planning, one who can help incorporate your Social Security claiming options into an overall retirement income plan.

Have You Thought about How Long You May Live in Retirement?

Have you ever thought about how many years you might spend in retirement? While we can't know for certain, we should think about how life expectancy has increased in the decades since Social Security began.

In 1935, life expectancy in the U.S. was 61.7 years.

By 2016 it had increased to 78.6 years. *

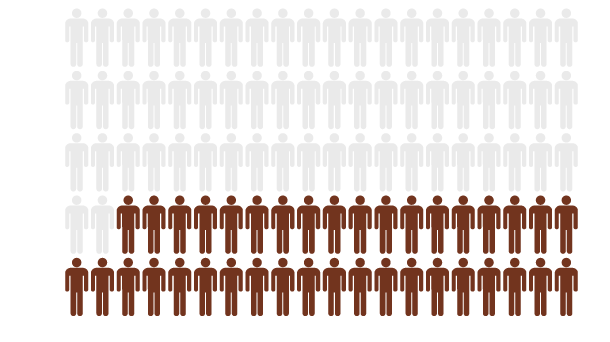

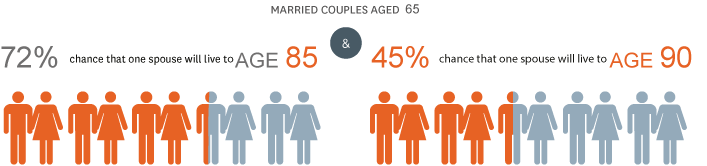

Consider a married couple age 65. There's a 72% chance that one spouse will live to age 85. And a 45% chance that one spouse will live to age 90. **

As of December 2017 ***, 5.7 million Social Security beneficiaries were at least age 85. Some much older. But collecting Social security benefits well into old age is nothing new.

Source: * Data Brief 293, 12/17

Source: ** Calculation based on mortality data from Society of Actuaries Retirement Participants 2000 table

Source: *** Social Security Administration Facts and Figures about Social Security, 2017

But Collecting Social Security Benefits Well Into Old Age Is Nothing New.

The very first person to collect Social Security retirement benefits was named Ida May Fuller.

A resident of Vermont, Ida May retired in 1939 after paying into Social Security for just three years. Ida May received her first Social Security payment on January 31, 1940. She then went on to collect from Social Security for thirty-five years.

Ida May passed away in 1975... at the age of one hundred.

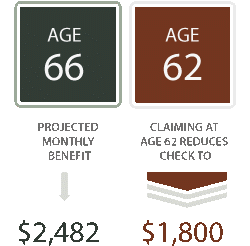

How Delaying May Boost Your Total Income

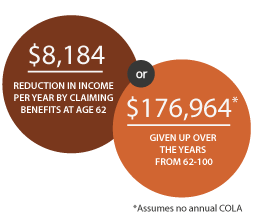

Let's assume that your age 66 projected monthly retirement benefit is $2,482. Claiming benefits at age 62 reduces the monthly check from $2,482, to $1,800.

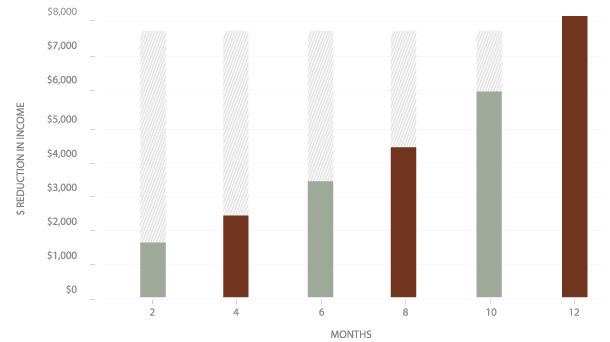

That's a reduction of $8,184 per year. Again, that reduction is not for a year, or a few years. It's PERMANENT.

Over the 38 years from age 62 until age 100, this means giving up one-hundred-seventy-six-thousand-nine-hundred-sixty-four-dollars.

Now, you may feel that living to age 100 is unrealistic. If so, then back that up by 20 years. If you were to live to age 80, the loss in retirement income is still $13,284.

Don't automatically think that claiming Social Security benefits early is your best decision.

It may have been the right choice for your parents, but it could be the wrong choice for you.

In fact, if you feel that you are likely to live to age 80, or, 85, you should think carefully about delaying benefits until even after your full retirement age. This is because for every year that you wait beyond full retirement age, your monthly check will be increased by an additional 8%.

Waiting until age 70 means receiving 32% more retirement income versus age 66, and 75% more income compared to age 62. That's $1,800 per month at age 62, versus $3,168 at age 70.

Although the difference in these two numbers is dramatic, it's only one factor in choosing the Social Security claiming strategy that's best for you.

The opportunity to receive a higher monthly income helps explain why proper retirement income planning is important. It also points out why a well-designed retirement income plan shouldn't overlook how to maximize Social Security benefits.

Your need for income and views about life expectancy are just two of many important factors in determining when to receive benefits.